November 2025 Sector SPDR Analyzer

Earnings season is off to a rough start, with high profile disappointments from firms in the Financial sector–often leading indicators–including J.P. Morgan (ETFs holding JPM), Morgan Stanley (MS) and Wells Fargo (WFC). But with those numbers now factored in to analysts’ forecasts, here’s a look at how Q2 earnings expectations for S&P 500 firms are stacking up.

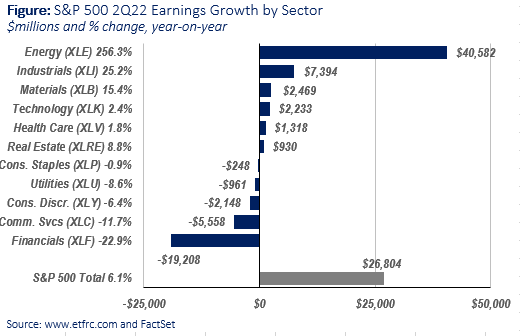

Overall, analysts forecast profit growth of $26.8 billion, about 6.1% YoY. That’s due entirely to the Energy sector (XLE), without which S&P 500 earnings would likely be down about 3.1%. Though oil prices have come down a bit lately, they are still much higher than they were a year ago making for easy comparisons. Meanwhile Financials (XLF) are expected to be the biggest drag on index profits, down around 23% YoY, and that’s before any further disappointments are factored in.

No other sector–despite anticipating profit growth of anywhere from negative 12% (Communication Services, XLC) to +25% (Industrials, XLI)–is expected to have as much of an impact on overall S&P 500 earnings growth. Even the Tech sector (XLK) is forecast to post only about 2% earnings growth YoY.

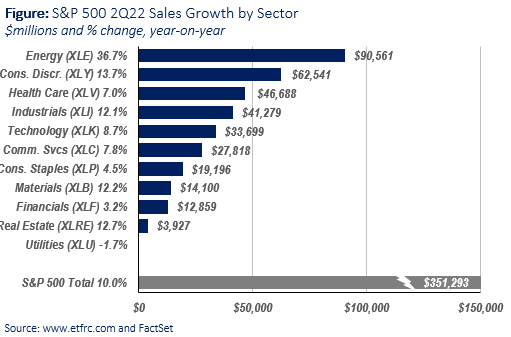

Revenue for S&P 500 firms is forecast to gain 10.0% YoY–less than one percentage point above inflation–and again driven by Energy. Excluding that sector, sales growth would be about 8.0%. All sectors, with the exception of Utilities (XLU) are anticipating revenue gains.

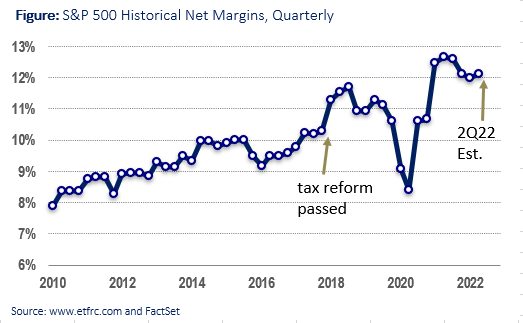

However you slice it, with earnings growing slower than the top line that means margins are under pressure, and down from the second quarter last year. Viewed over the longer term however, margins remain exceptionally robust.

Just as important as how Q2 earnings reports come in will be guidance given by company managements for the rest of the year, particularly since we appear to be on the verge of an earnings recession. The typical pattern is for companies to “beat then lower” (i.e., beat consensus expectations but then lower forward guidance to a number they believe they can beat again). But with the economy weakening and only single-digit earnings growth forecast for the 3rd and 4th quarters, there is little room for error before the conversation turns from earnings growth to earnings declines.

As always, you can stay on top of changing forecasts as well as daily changes in valuations (P/E ratios etc.) based on those forecasts, by visiting the Fund Focus page for the S&P 500 SPDR (SPY), as well as each Sector SPDR ETF’s focus page for a more granular look. Each month we also publish the Sector SPDR Analyzer (July 2022 edition), which you can receive automatically by joining ETF Research Center as a Basic (free) member.

Related posts